Unpacking the Reality: How an Increasing-Cost Industry Shapes Our World

The economic landscape is a complex and ever-shifting terrain. Within this intricate system, certain industries operate under unique pressures, one of the most significant being the characteristic of an increasing-cost industry. This article delves into the intricacies of this phenomenon, exploring its defining features, identifying prominent examples, and analyzing its profound impact on businesses, consumers, and the global economy.

Understanding an increasing-cost industry is crucial for anyone seeking to navigate the complexities of the modern market. It’s not merely a technical concept; it’s a force that shapes prices, influences investment decisions, and ultimately, dictates the availability and affordability of essential goods and services. This exploration will unravel the mechanisms driving these industries and illuminate the challenges and opportunities they present.

Defining the Increasing-Cost Industry

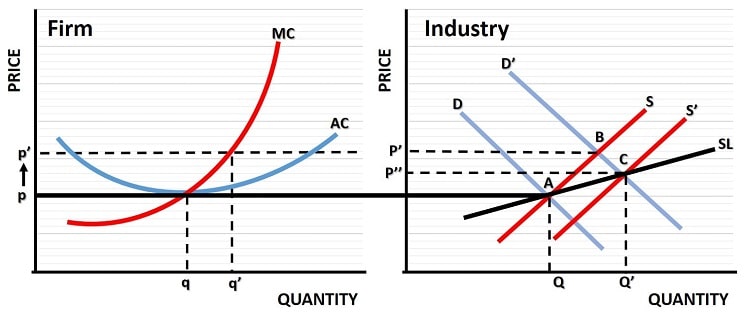

At its core, an increasing-cost industry is associated with a situation where the average production costs for individual firms rise as the overall industry output expands. This contrasts with decreasing-cost industries, where economies of scale lead to reduced costs as production increases, and constant-cost industries, where costs remain relatively stable regardless of output. The defining characteristic of an increasing-cost industry is the upward pressure on costs as the industry grows.

Several factors contribute to this cost escalation. One primary driver is the limited availability of essential resources. As an industry expands, it may face increasing competition for these resources, driving up their prices. For example, consider a construction industry that heavily relies on specific types of land or skilled labor. As the industry grows, the demand for these limited resources increases, causing their prices to rise and, consequently, increasing the overall production costs for construction firms.

Another significant factor is the diminishing returns on investment in certain areas. As an industry expands, it may need to tap into less efficient resources or locations, leading to higher costs. This is particularly evident in industries that depend on natural resources. As the industry extracts the most easily accessible and high-quality resources, it must move to less accessible and lower-quality sources, inevitably increasing the costs of extraction and processing.

Identifying Industries Facing Increasing Costs

Several industries are characteristically associated with increasing costs. Recognizing these industries is key to understanding the economic forces at play. Here are some prominent examples:

- Agriculture: The agricultural sector often experiences increasing costs, particularly in areas with limited arable land or water resources. As the demand for food rises, farmers may need to cultivate less fertile land or invest in expensive irrigation systems, leading to higher production costs. Furthermore, the increasing cost of fertilizers, pesticides, and labor can significantly impact farming expenses.

- Mining: Mining operations are frequently impacted by increasing costs. As easily accessible mineral deposits are depleted, mining companies must venture into more remote and challenging locations, requiring more complex and expensive extraction techniques. The cost of labor, specialized equipment, and environmental compliance also contributes to rising costs.

- Oil and Gas Extraction: Similar to mining, the oil and gas industry often faces increasing costs. As readily available reserves are exhausted, companies must explore and extract from deeper waters, more challenging terrains, or utilize more advanced and costly extraction methods like fracking. This, coupled with the fluctuating prices of equipment and labor, drives up production expenses.

- Construction: The construction industry is highly sensitive to the prices of raw materials like lumber, steel, and cement. As the demand for construction rises, the prices of these materials often increase. Moreover, the competition for skilled labor in the construction sector can drive up wages, contributing to the increasing-cost dynamics.

- Real Estate Development: As urban areas become more developed, the cost of land increases. Furthermore, the cost of labor and materials for construction increases, making this another industry that is characteristically associated with increasing costs.

Impact on Businesses and Consumers

The characteristics of an increasing-cost industry have far-reaching consequences for both businesses and consumers. Businesses operating in these industries face significant challenges in maintaining profitability and competitiveness. They must carefully manage their costs, seek innovative solutions to improve efficiency, and potentially pass on increased costs to consumers.

For businesses, the rising costs can squeeze profit margins, particularly during periods of economic downturn when demand may be weak. This can lead to reduced investment, slower growth, and even business failures. In response, companies may explore various strategies, including:

- Investing in technology: Automation and other technological advancements can help improve efficiency and reduce labor costs.

- Seeking alternative resources: Diversifying suppliers and exploring alternative materials can help mitigate the impact of rising resource prices.

- Consolidation: Mergers and acquisitions can create economies of scale and improve bargaining power with suppliers.

- Price adjustments: Passing on increased costs to consumers, though this may be limited by market competition and consumer sensitivity.

Consumers are also affected by the characteristics of an increasing-cost industry. Higher production costs often translate into higher prices for goods and services. This can reduce consumer purchasing power and lead to decreased demand. Consumers may respond by:

- Reducing consumption: Cutting back on discretionary spending or postponing purchases.

- Seeking cheaper alternatives: Switching to lower-priced brands or products.

- Delaying purchases: Waiting for prices to fall or for better deals.

The Role of Government and Policy

Government policies can play a significant role in influencing the dynamics of an increasing-cost industry. Policies that promote resource conservation, encourage technological innovation, and foster competition can help mitigate the impact of rising costs. Conversely, policies that create artificial barriers to entry or distort market signals can exacerbate the problem.

Government interventions can take various forms, including:

- Subsidies: Providing financial assistance to businesses to offset rising costs, such as subsidies for renewable energy or sustainable farming practices.

- Regulations: Implementing regulations to promote resource efficiency, environmental protection, and fair labor practices.

- Infrastructure development: Investing in infrastructure, such as transportation networks and energy grids, to reduce transportation costs and improve access to resources.

- Tax policies: Implementing tax policies that encourage investment in innovation and efficiency.

Navigating the Challenges and Opportunities

Understanding the characteristics of an increasing-cost industry is vital for businesses, consumers, and policymakers alike. Businesses must adapt their strategies to manage rising costs and maintain competitiveness. Consumers need to be aware of the impact of these industries on prices and make informed purchasing decisions. Policymakers must implement effective policies to promote sustainable growth and mitigate the negative consequences of rising costs.

The increasing-cost industry presents both challenges and opportunities. While it can lead to higher prices and reduced consumer purchasing power, it also incentivizes innovation, efficiency, and resource conservation. Businesses that can adapt to rising costs and find ways to improve efficiency will be well-positioned to thrive in these industries. Consumers who make informed choices and support sustainable practices can help drive positive change. Policymakers who implement sound policies can help ensure that these industries contribute to a more sustainable and prosperous future.

The Future of Industries with Increasing Costs

Looking ahead, the characteristics of an increasing-cost industry will likely become even more prominent. Factors such as climate change, resource scarcity, and rising labor costs are expected to exert further upward pressure on production expenses. This underscores the importance of proactive strategies to address the challenges and seize the opportunities presented by these industries.

Technological advancements, such as automation, artificial intelligence, and renewable energy technologies, offer promising solutions for improving efficiency and reducing costs. Investment in research and development, coupled with supportive government policies, will be crucial for driving innovation and creating sustainable solutions. Furthermore, fostering collaboration between businesses, governments, and consumers will be essential for navigating the complexities of an increasing-cost industry and building a more resilient and prosperous future. The key is to understand that an increasing-cost industry is associated with inherent challenges, but also a potential for innovation and sustainable growth.

The economic landscape is constantly evolving, and the characteristics of an increasing-cost industry are a critical element in this evolution. By understanding the forces at play, businesses, consumers, and policymakers can make informed decisions and contribute to a more sustainable and prosperous future. This understanding is not just about economics; it is about shaping a world where resources are used efficiently, innovation flourishes, and the needs of both current and future generations are met. The impact of an increasing-cost industry is far-reaching, and its significance will only continue to grow in the years to come.

[See also: Related Article Titles]